On rental “investment” property

I found this an interesting read from seeking alpha. I have had many discussions with folks regarding real estate, particularly rental real estate. From my observations, real estate is an overly-emotional transaction. The seeking alpha article below takes a step back and examines some of the facts of purchasing Real Estate Investment Trusts (REITs) vs. rental property. I say “some” of the facts because the article omits the following critical costs of rental property ownership:

- Property taxes.

- That depreciation expense you take every year ultimately translates into repairs. “The chickens will come home to roost” so to speak. You depreciate $10,000 this year, eventually an AC or roof or fence or whatever needs to be repaired. And those expenses persist once you have exhausted all of your deprecation allowance.

- Insurance costs for rentals is higher than owner-occupied homes. Take a look at this 2022.10.14 article from Benzinga (via yahoo finance) titled “Insurance Costs Are Rising, But Real Estate Investors Could Lose More By Not Being Honest About Their Property”: HTML.

- What about vacancies? Many rental property owners assume properties will be rented 365 days year. That is simply untrue. And with turnover comes costs.

Myth: home prices always go up

While I am at it, let me share a couple charts to address the myth that “home prices always go up.” First, the S&P CoreLogic Case-Shiller home price index from 1986.01.01 to 2022.07.31:

Figure 1: S&P CoreLogic Case-Shiller US Home price index from 1986.01.01 to 2022.07.31. Source: Bloomberg.

We are all familiar with the Great Recession and subprime mortgage crisis around 2008. Figure 1 shows home prices dropped 26.76% from the 2006.06.30 peak to the 2011.12.30 low. Also note the incredible spike in prices towards the end of the data sample. This is not sustainable.

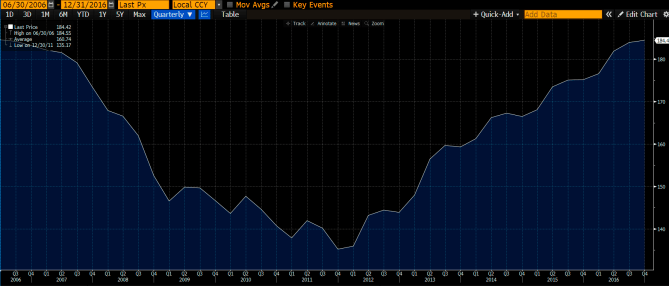

So how long did it take for home prices to reach their 2006.06.30 peak? Over ten years:

Figure 2: S&P CoreLogic Case-Shiller US Home price index from 2006.06.30 to 2016.12.31. Source: Bloomberg.

On home affordability

A recent NPR article titled “With mortgage rates near 7%, the housing party is over. Now it’s hangover time” (HTML) provides examples of folks stretching their budgets to overpay for a home they truly can not afford. This relates to emotions involved in home purchases (be it rental or for your primary residence). Dave Ramsey has three simple criteria to assess whether or not you can truly afford the home you wish to purchase (HTML):

- 15 year fixed rate mortgage.

- 20% down payment.

- All-in monthly home payment less than 25% of take-home pay.

How many actually go through those calculations? How many disregard the results even if they did do the calculation? How many changed the 15 year term to 30, 40, or more years just so they could “afford” a more expensive house?

In conclusion, be careful when describing your real estate purchase as an “investment.” If you do the math, which means including ALL costs (insurance, vacancies, repairs, property taxes, real estate commissions when you sell, closing costs when you buy, etc.) you may see: (1) you couldn’t afford the home in the first place, (2) it was a poor investment, and (3) there are many better alternatives.

-Dr. Moore

Pingback: Figures for that previous post… | Efficient Minds™

I’ve been investing in REITs because that’s what I can afford. I don’t have money for 20% down on an investment property although I’m hoping to get there. REITs are quite easy, and I’m not in love with the idea of being a landlord, but….I’m very attracted to thought of owning more than one property in the area where I live. I think it will create value for me and my family.