“Only poor people believe they need alpha they cannot afford to become wealthy.

Wealthy people can become poor chasing alpha but remain wealthy with beta.” -Dr. Moore

Simplified definitions for that quote:

alpha = returns above a simple index fund (e.g., S&P500 fund like VOO)

beta = returns of a simple index fund (e.g., S&P500 fund like VOO)

You are not special.

There is voluminous research documenting the poor performance of IPOs. But to keep this post brief, I will quote from Jensen and Jensen (2025), a textbook I use for my Investments and Modern Portfolio Managementclasses:

…the average investor typically cannot receive an initial allocation of “hot” stocks because the investment bankers reward favored clients with shares. (p. 86, emphasis added)

A tale of two starting prices. A couple important definitions:

- Offering price = the price paid by the investment bank and their privileged clients. In the case of SpaceX (SPCX), this was $135.

- Opening price = the price of the first trade on a given day. In the case of SPCX, this was $150.

To be clear, the $135 Offering price for the “initial allocation” did not go to folks purchasing via their brokerage apps (Robinhood, Fidelity, Interactive Brokers, whatever) – that was only for the privileged few. Everyone else paid the $150+ Opening price.

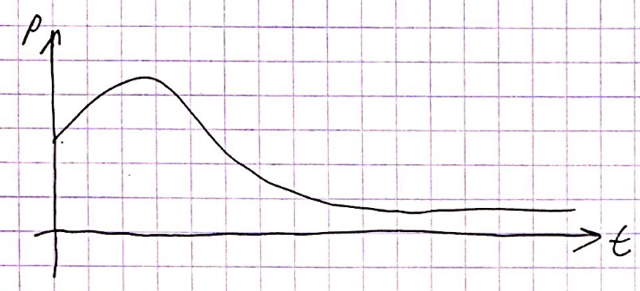

IPO price patterns

So the Jensen and Jensen (2025) textbook is clear, IPOs underperform. Here is the price pattern of IPOs taught to me by Professor Lemmon at Arizona State University way back in 1999 while working towards my MBA degree:

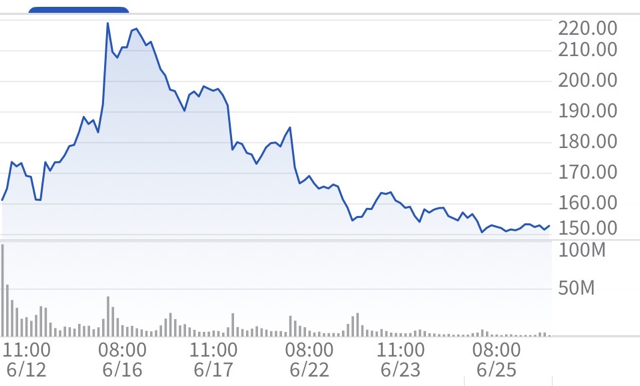

And what do we see in SPCX’s price pattern as of now?:

(Source: IBKR app, 2026.06.26 around 7:25AM)

I have many more examples like this of prior IPOs. Professor Lemmon does as well. So does Jay Ritter…

The research on IPO performance. Again, I quote Jensen and Jensen (2025):

Dr. Jay Ritter, an authority on IPOs, finds that the average three-year return of IPO stocks lag that of similar non-IPO stocks by a significant margin. He attributes this to fads and irrational optimism on the part of investors. Thus, you are lucky if you can obtain an initial IPO allocation, but you probably should avoid purchasing recent IPO stocks in the secondary market. (p. 87, emphasis added)

To be clear, the secondary market is where the majority trade and paid the $150+ opening price after the privileged few paid $135 offering price in the primary market. You can map my alpha and beta definitions to Ritter’s empirical evidence: beta (non-IPO stocks, e.g., simple S&P 500 Index fund) outperforms alpha (IPO stocks).

Looking at the SPCX stock chart, you see many purchased SPCX for over $200 in the secondary market. They were caught up in the “fads and irrational optimism”. Those who purchased at the peak lost 1/3rd of their investment in just two weeks.

SpaceX artificial demand and optimism generation

SpaceX has at least six peculiarities that artificially inflate demand to hype up their stock.

- Rapid confidential S-1 filing process. See SpaceX’s Record 74-Day IPO: Can OpenAI and Anthropic Replicate SpaceX’s Capital Miracle? HTML. Let this be a warning to those considering jumping on the OpenAI and Anthropic IPO hype trains.

- Fast-tracked index inclusion. Several indexes changed their rules so that SPCX could be added early. As a result, several index funds must purchase SPCX stock. But not all indexes and index funds. See SpaceX Faces Delay to S&P 500 Inclusion After Index Provider Keeps Existing Criteria: HTML.

- Extremely small float. See SpaceX’s ‘puny free float’ is sparking concerns about greater stock volatility: HTML. Less float (shares avialable to trade), more [artificially induced] demand.

- Minimal media discussion of actual float-adjusted index weight. Although the headlines suggest lots of index funds are buying lots of SPCX stock, the reality is more nuanced. Importantly, S&P500 stuck to its rules. The S&P500 index fund is the major US Equity index fund in CalPERs and perhaps most pension funds and 401(k) plans. So the concern that “I’m forced to buy SPCX” is likely untrue for most. See Morningstar.com’s The SpaceX IPO: How Index Funds Are Adapting for more detail: HTML.

- Minimal media coverage of operating losses. See SpaceX Stock Is Down 16.4% – and the Real Selling Hasn’t Even Started: HTML. Allow me to quote: “SpaceX posted $18 billion in 2025 revenue but a $4.9 billion net loss, per Morningstar’s analysis of the S-1.” Note: the S-1 filing occurred before the IPO. SpaceX also just took out a $20 billion dollar loan to which that same article states: “Locking in billions in ongoing interest expense while still posting net losses is like financing a kitchen renovation the week your freelance contracts dry up.”

- Complicated lockup / release terms. Again, see SpaceX Stock Is Down 16.4% – and the Real Selling Hasn’t Even Started: HTML. You may read it for yourselves. But very soon insiders will be able to cash out putting downward pressure on the price. As the article states: “The Unlock Calendar Is the Real Problem.”

Conclusion

Many have already lost money on the SPCX IPO. Many have lost money on IPOs in the past. The empirical (and even theoretical) research is clear. So why do many retail (Robinhood, Fidelity, etc. account holders) traders still get involved? I conclude with a quote from Bagehot (1971) who may have this correct:

…people presumably participate in the stock market because, like parlor games and sports, it offers the opportunity to win more dramatically and more concretely than is possible in ordinary workaday life.

But don’t forget: It also offers the opportunity to lose more dramatically and concretely. And the data suggest that is the more likely outcome with IPOs.

-Dr. Moore

References

Bagehot, W. (1971). The Only Game in Town. Financial Analysts Journal, 27(2), 12–22. https://doi.org/10.2469/faj.v27.n2.12

Jensen, G. R., & Jensen, T. K. (2025). Investments : analysis and management (Fifteenth edition.). Wiley.