Some philosophy first…

“Without truth, there is only manipulation” -Os Guinness

I have long been skeptical of Tesla’s stock valuation. As a result, I never purchased TSLA stock (entered a long position) either directly or through the S&P500 Index fund of which TSLA is not a member. By the way, why isn’t Tesla in the S&P 500: “The reason is simple: it hasn’t been profitable long enough.”: HTML. More on “profitable” later in this post.

I have never entered a short position on TSLA either for two reasons. One, I’m just too risk averse (chicken). Second, I recently read this quote from the Dhammapada:

“Don’t try to build your happiness on the unhappiness of others. You will be enmeshed in a net of hatred.”

Perhaps there is a lesson for the Trump Administration in there, but I digress. Getting back to the title of the article, does Tesla manipulate financial markets?

Manipulation mechanics

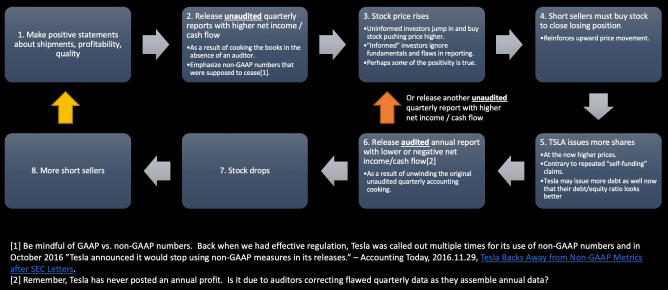

To begin, I assembled the following diagram to illustrate the feedback loop of positive statements (be it qualitative or quantitative), unaudited quarterly reports, uniformed investors jumping in, informed investors ignoring fundamentals and unaudited statement flaws, short squeezes, and inflated prices.

Figure 1. One perspective on TSLA [over]valuation

Figure 1. One perspective on TSLA [over]valuation

Fig. 1 shows short-sellers (blocks #3 and #4) are experiencing the karma of that Dhammapada quote. Here is my friendly suggestion for folks out there: if you like the stock, buy it. If you don’t like it, don’t buy it (or sell it if you already have it). If you short it, your are attempting to build your happiness (profit) on the unhappiness of others (stock price drop).

The irony in Fig. 1 is that the price of Tesla rises as short-sellers are forced to close their positions by purchasing Tesla stock (block #4). That purchasing adds further upward pressure on the price forcing other short-positions to lose money and the cycle continues. Figure 2 shows that although short-sellers were winning (and piling on) from February 2019 until June 2019, they started losing and closing their positions thereafter.

Figure 2. TSLA short interest (white) vs. market capitalization (green). Source: Bloomberg.

Figure 2. TSLA short interest (white) vs. market capitalization (green). Source: Bloomberg.

Let’s look a little deeper at the situation through the lens of Fig. 1.

Figure 1, Block 1: Qualitative manipulation via claims of profitability

Traditionally credible prospects of attainable earnings growth, dividend payment growth, or stock repurchases leads to price increases. In the case of Tesla, there are no dividends and actually the opposite of stock repurchases: continual share and debt issuances (Fig. 1, block #5).

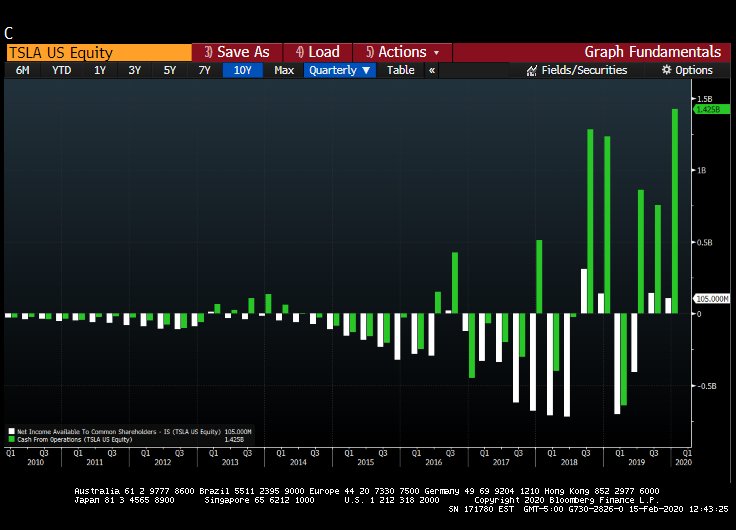

How do the claims of profitability line up with the financial reports? Figures 3 and 4 show unaudited quarterly and audited annual results (more on unaudited vs. audited later).

Figure 3. Quarterly net income (white) and operating cash flow (green) over time. Source: Bloomberg Terminal.

Figure 3. Quarterly net income (white) and operating cash flow (green) over time. Source: Bloomberg Terminal. Figure 4. Annual net income (white) and operating cash flow (green) over time. Source: Bloomberg Terminal.

Figure 4. Annual net income (white) and operating cash flow (green) over time. Source: Bloomberg Terminal.

Looking at Figures 3 and 4 I wonder how Tesla can go from negative $1 billion in net income to positive $2 billion in operating cash flow in 2018 and 2019? It looks fishy, especially given the historical data, both unaudited quarterly or audited annual data. Perhaps this is related to the 2020.02.13 disclosure in Tesla’s 10-K that the SEC issued a subpoena on 2019.12.04 for “certain financial data and contracts including Tesla’s regular financing arrangements”: HTML.

Speaking of auditing, there is another concern brought to my attention by my accounting colleague. Here is a quote:

“The Trump administration has indicated it plans to abolish the Public Company Accounting Oversight Board (PCAOB), the US audit regulator, and roll its functions into the Securities and Exchange Commission (SEC) in its budget blueprint, although immediate action is unlikely.”

Source: Accountancy Daily 2020.02.14: HTML.

I see this as a broader deregulation push that can (and likely will) harm investors, consumers, etc. More on deregulation in the GAAP vs. non-GAAP section later in this post.

I now move on to self-funding claims.

Figure 1, Block 5: Qualitative manipulation via claims of self-funding / self-sustainability

Tesla repeatedly claims to be “self-funding” or “self-sustaining” while continually raising funding from equity markets (stock issuances) and debt markets. I present the claims from Tesla followed by a graph that shows evidence to the contrary (Figure 5).

“Tesla does not need to ever raise another funding round” -Tesla CEO Elon Musk in 2012: HTML.

Then, Tesla announces in 2019 that it will raise $2 billion in debt and equity markets:

“Years go by and a self-sustaining Tesla eludes Elon Musk” – LA Times 2019.05.02 article: HTML.

Or even as recently as the January 29, 2020 conference call:

“it doesn’t make sense to raise money, because we expect to generate cash despite this growth level.” -Elon Musk January 29, 2020 conference call: HTML.

But guess what happened just 15 days after making that statement? Tesla announces another $2 billion stock issuance: HTML. It turns out this is nothing new. Tesla issued stock and debt continually since its inception (Fig. 5). Note that some of the issuances are related to stock-based employee compensation (read: that in effect lets market participants pay Tesla employees rather than having a drag on Tesla’s cash).

Figure 5. Tesla shares outstanding (top) and total debt (bottom) over time. Source: Bloomberg Terminal.

Figure 5. Tesla shares outstanding (top) and total debt (bottom) over time. Source: Bloomberg Terminal.

So profitability claims are suspect (Figures 3 and 4) while self-funding claims are demonstrably false (Figure 5).

Figure 1, Blocks 2 and 6: Quantitative manipulation via the use of non-GAAP numbers

Ever wonder why Tesla has never had a profitable annual report while having some “profitable” quarterly reports? Two things come to mind: (1) annual reports are audited while quarterly reports are unaudited and (2) the use and emphasis of non-GAAP numbers by corporations such as Tesla.

There are earnings based on Generally Accepted Accounting Principals (GAAP) that companies must follow: HTML. Then there are company “adjusted” and reported “non-GAAP” numbers. In Tesla’s case, let’s go back to August 2016:

“The SEC chided the Palo Alto, California-based electric car maker [Tesla] for employing ‘individually tailored’ metrics in an earnings release this past August and has raised the issue with the company in four separate letters between mid-September and mid-October, according to The Wall Street Journal. In October, Tesla announced it would stop using non-GAAP measures in its releases.” -Accounting Today, 2016.11.26, Tesla Backs Away from Non-GAAP Metrics after SEC Letters

Back then regulation seemed important. These days, under the Trump administration, we see an environment of deregulation. This is evidenced by the recent plans to abolish the PCAOB which regulates the auditors of such financial statements: HTML. While in a deregulation environment, why not go back to your old ways of posting non-GAAP numbers? Figure 6 shows a page from Tesla’s own January filing:

Figure 6. Excerpt from Tesla’s 2020.01.29 8-K filing.

Figure 6. Excerpt from Tesla’s 2020.01.29 8-K filing.

I’m not sure how that comes out here on WordPress, but let me highlight GAAP vs. non-GAAP (also note “unaudited” in top left corner of Tesla’s filing):.

- Net Income Q42019 (GAAP) = 105 million, QoQ -27%, YoY -25%

- Net Income Q42019 (non-GAAP) = 386 million, QoQ +13%, YoY +12%

- EPS Q42019 (GAAP) = 0.58, QoQ -28%, YoY -28%

- EPS Q42019 (non-GAAP) = 2.14, QoQ +12%, YoY +7%

So clearly, non-GAAP numbers look better than GAAP numbers. But didn’t Tesla respond to the SEC 4 years ago (HTML) saying they were going to stop non-GAAP metrics? Again, emphasis on non-GAAP measures draws in uninformed investors (pushing the price up), pressures short-sellers to close their position (further pushing the price up), then Tesla issues more shares at the higher prices.

Conclusion

Figure 1 illustrates a feedback loop that can help explain the extreme rise in TSLA stock. Figure 2 shows how the feedback loop has played out in the market via increased prices causing short squeezes. I presented qualitative statements from Tesla regarding profitability and self-funding and empirical evidence to the contrary (Figures 3, 4, and 5). I noted the role of the deregulatory environment that can lead to investor harm. I conclude by saying I don’t know what TSLA stock is worth. I am not licensed to provide financial advice in any jurisdiction on Earth. 🙂

-Dr. Moore

I almost forgot… Tulips!

Just go read the Tulip Mania Wikipedia page when you are bored: HTML.